For more than a decade, a UAE invoice could be a PDF attached to an email, a printout handed across a desk, or a line in a spreadsheet. That era is ending. The Ministry of Finance and the Federal Tax Authority are moving the entire UAE onto a structured, machine-readable electronic invoicing system that transmits transaction data to the FTA in near real time. If your business operates in the UAE — mainland, free zone, or otherwise — this is the single most significant compliance change since VAT arrived in 2018. And unlike VAT, which gave businesses a relatively long runway, the first mandatory deadline for large businesses is 1 January 2027. The pilot opens 1 July 2026. The window to prepare is short.

This article is based on the official legislative framework — Ministerial Decisions No. 243 and 244 of 2025 from the Ministry of Finance, the Federal Tax Authority e-Invoicing guidance, and the technical documentation published by the FTA in February 2026 — supplemented by analysis from KPMG, Deloitte, and other leading advisory firms. I will tell you exactly what the system is, who it applies to, what you need to do, and when you need to do it.

- What UAE e-Invoicing Actually Is

- Why the UAE Is Doing This Now

- The Legal Framework — Ministerial Decisions 243 and 244

- Who Must Comply — Scope and Exclusions

- The Peppol PINT AE Standard and the 5-Corner Model

- Accredited Service Providers — What They Are and Why You Need One

- The Rollout Timeline — Phase by Phase

- What Makes a Valid UAE e-Invoice

- Penalties for Non-Compliance

- Your Practical Action Plan

- Frequently Asked Questions

What UAE e-Invoicing Actually Is

The UAE e-Invoicing system replaces PDFs and paper with structured XML invoices transmitted through an Accredited Service Provider to the FTA near real time.

UAE e-Invoicing is not simply sending an invoice by email rather than post. It is a fundamentally different mechanism. Under the UAE Electronic Invoicing System, invoices must be generated in a structured XML format, transmitted through a government-approved Accredited Service Provider, and reported to the FTA's system in near real time. A PDF sent by email does not qualify. A scanned paper invoice does not qualify. A Word document does not qualify. The invoice must be machine-readable, structured according to specific technical standards, and flow through an authorised network before it reaches your buyer.

The system operates on what the UAE has called a Continuous Transaction Control and Exchange model — meaning the FTA receives invoice data at the time of issuance, not after the fact in a periodic return. This is a significant shift in how the UAE tax authority sees and audits commercial activity. Instead of reconciling invoices after a tax period, the FTA will have near real-time visibility into your B2B and B2G transactions.

Everything in this article derives from the primary official documentation. The core legal instruments are Ministerial Decision No. 243 of 2025 (the Electronic Invoicing System) and Ministerial Decision No. 244 of 2025 (implementation framework and accreditation), both issued by the Ministry of Finance on 28 September 2025. The FTA published supplementary technical guidance on required data fields in February 2026. For the primary source, always refer to tax.gov.ae and mof.gov.ae/e-Invoicing.

Why the UAE Is Doing This Now

The UAE has moved through a clear sequence of tax reforms. Excise tax arrived in 2017. VAT followed in 2018. Corporate income tax commenced in 2023. e-Invoicing is the next logical step, and it is driven by a combination of policy objectives that have been building for several years.

The primary driver is tax compliance and audit efficiency. With e-Invoicing, the FTA receives invoice data almost instantly. This closes the gap between what businesses report in their VAT returns and what they actually transact — a gap that creates opportunities for under-reporting, fictitious invoices, and VAT fraud. Real-time data reporting makes those practices significantly harder to sustain and significantly easier to detect.

The second driver is the UAE's broader ambition to position itself as a leading digital economy. The UAE Vision 2031 and the National Digital Economy Strategy both commit the country to digitising core business processes. Moving commercial invoicing into a structured, automated, data-driven environment is entirely consistent with that direction. It also reduces businesses' reliance on manual, paper-based processes — which benefits everyone over time, even if the transition requires effort upfront.

The third driver is international alignment. The UAE has adopted the Peppol network, which is the same international framework used by the EU, Singapore, Australia, and a growing number of countries for structured invoice exchange. Aligning with Peppol makes UAE invoice data interoperable with international standards, reduces friction for businesses trading across borders, and positions the country within a recognised global compliance framework.

The Legal Framework — Ministerial Decisions 243 and 244

The UAE Ministry of Finance issued the two Ministerial Decisions on 28 September 2025 that establish the complete legal and operational framework for e-Invoicing.

The legal foundations were laid in two steps. First, Federal Decree-Law No. 16 of 2024 amended the VAT Law to formally define electronic invoicing and establish its place within the UAE tax framework. Federal Decree-Law No. 17 of 2024 amended the Tax Procedures Law to define the role of Accredited Service Providers and the obligations of businesses using them. These amendments created the legislative authority for what followed.

On 28 September 2025, the Ministry of Finance issued the two key operational instruments:

Ministerial Decision No. 243 of 2025 — The Electronic Invoicing System. This decision establishes the scope of the mandate — who it applies to, what transactions are covered, what types of electronic documents must be exchanged, and the overarching obligations of issuers and recipients. It also sets out the exclusions: sovereign government activities not in competition with the private sector, certain international airline transport services, certain exempt financial services, and B2C (business-to-consumer) transactions, which remain out of scope until further notice.

Ministerial Decision No. 244 of 2025 — Implementation Framework and Accreditation. This decision establishes the phased rollout timeline, the requirements for businesses at each phase, the accreditation process for service providers, and the technical data dictionary (known as the PINT AE Data Dictionary) that defines the mandatory fields every e-Invoice must contain. It also specifies the pilot programme structure and the obligations of businesses that choose to participate before the mandatory dates.

In February 2026, the FTA published a 16-page technical document providing the complete set of required data elements for both electronic tax invoices and commercial electronic invoices in XML format, aligned with the final PINT AE specifications. KPMG's analysis of this document is among the most thorough available for businesses planning their implementation.

Who Must Comply — Scope and Exclusions

The e-Invoicing mandate applies to all persons conducting business in the UAE for B2B and B2G transactions — whether or not they are VAT-registered. This scope is deliberately wider than VAT itself. If you are below the VAT registration threshold but you conduct B2B transactions, you are still potentially in scope. Do not assume that being VAT-exempt or non-VAT-registered excludes you. Assume you are in scope and verify any specific exclusion that might apply to your situation.

The mandate covers every business operating in the UAE — mainland and free zones — for their business-to-business (B2B) and business-to-government (B2G) transactions. Deloitte's analysis confirms that businesses in all major UAE free zones — DIFC, DMCC, JAFZA, ADGM, and others — are subject to the same phased mandate as mainland businesses. The FTA has made clear that no exemptions will be granted based on emirate, location, or jurisdiction type.

The following are specifically excluded under Ministerial Decision 243 of 2025:

In Scope

- All B2B transactions for UAE businesses (VAT-registered or not)

- All B2G transactions with UAE government entities

- Free zone companies (DIFC, DMCC, JAFZA, ADGM, and all others)

- Businesses operating across all seven emirates

- Foreign businesses conducting business in the UAE

- Intra-group transactions (with a 24-month grace period from 1 January 2027)

Excluded or Deferred

- B2C (business-to-consumer) transactions — excluded until further notice

- Sovereign government activities not in competition with the private sector

- Certain international airline passenger and cargo transport services

- Certain exempt financial services qualifying for specific treatment

- Intra-group VAT transactions — 24-month grace period from January 2027

- Other categories the Minister of Finance may designate over time

The Peppol PINT AE Standard and the 5-Corner Model

The UAE has adopted the Peppol 5-Corner Model. Invoices flow from your system through your ASP (Corner 2), to your buyer's ASP (Corner 3), to your buyer (Corner 4), with Tax Data Documents reported to the FTA (Corner 5) at each stage.

The UAE has adopted the Open Peppol network as its technical infrastructure for e-Invoicing. Peppol — Pan-European Public Procurement OnLine — is an internationally recognised framework for structured invoice exchange originally developed for the EU public sector and now used in over 40 countries. The UAE's adoption of Peppol creates interoperability with international trading partners who are already on the network.

The specific technical standard the UAE uses is called PINT AE — Peppol International for the UAE. It is a localised version of the international Peppol Invoice specification, adapted to reflect UAE VAT law, Arabic language requirements, and the specific data fields the FTA requires. Invoices must conform to the PINT AE XML schema — a structured data format that your accounting or ERP system must be capable of producing or exporting.

The UAE has implemented what is called a 5-Corner Model. This is how an e-Invoice flows through the system:

Corner 1 — You (the Supplier): Your accounting system generates the invoice in PINT AE XML format and submits it to your ASP.

Corner 2 — Your ASP: Your Accredited Service Provider validates the invoice against FTA requirements and transmits it through the Peppol network. It also sends a Tax Data Document (TDD) to Corner 5.

Corner 3 — Buyer's ASP: Your customer's Accredited Service Provider receives the invoice, validates it, sends a Message Level Status back to your ASP, and also reports the TDD to Corner 5.

Corner 4 — Your Buyer: The buyer receives the validated invoice from their ASP in the format they have agreed.

Corner 5 — The FTA: The FTA's e-Billing system receives the Tax Data Documents from both ASPs, giving the authority near real-time visibility into the transaction. If validation fails at any point, no TDD is reported and the parties receive an error status.

Your Tax Identification Number (TIN) — specifically the first 10 digits of your corporate tax registration number — serves as your Peppol Participant Identifier in this network. This is how the system knows who you are and routes your invoices correctly.

Accredited Service Providers — What They Are and Why You Need One

An Accredited Service Provider is a technology company that has been approved by the FTA to operate as a corner in the Peppol network for UAE e-Invoicing. You cannot submit e-Invoices to buyers or to the FTA directly. Every invoice must pass through an ASP. This is not optional — it is structural to how the system works.

Your ASP does several things for you. It receives the XML invoice data from your accounting or ERP system, validates it against the PINT AE specification and the FTA's mandatory field requirements, transmits it through the Peppol network to your buyer's ASP, reports the Tax Data Document to Corner 5 (the FTA), and returns a Message Level Status to confirm whether the exchange was successful. If your invoice fails validation — because a mandatory field is missing, or a code is incorrect — your ASP will return an error and the invoice will not be delivered or reported until the issue is corrected.

Choosing the right ASP matters. The ASP list accredited by the FTA will be published on the official FTA website at tax.gov.ae. When evaluating an ASP, consider: compatibility with your existing ERP or accounting system, their integration approach, the support they offer during implementation, their pricing model, and their capacity given that all large businesses in the UAE will be appointing ASPs within a very short window. ClearTax's technical guide provides a useful overview of what to assess in an ASP relationship.

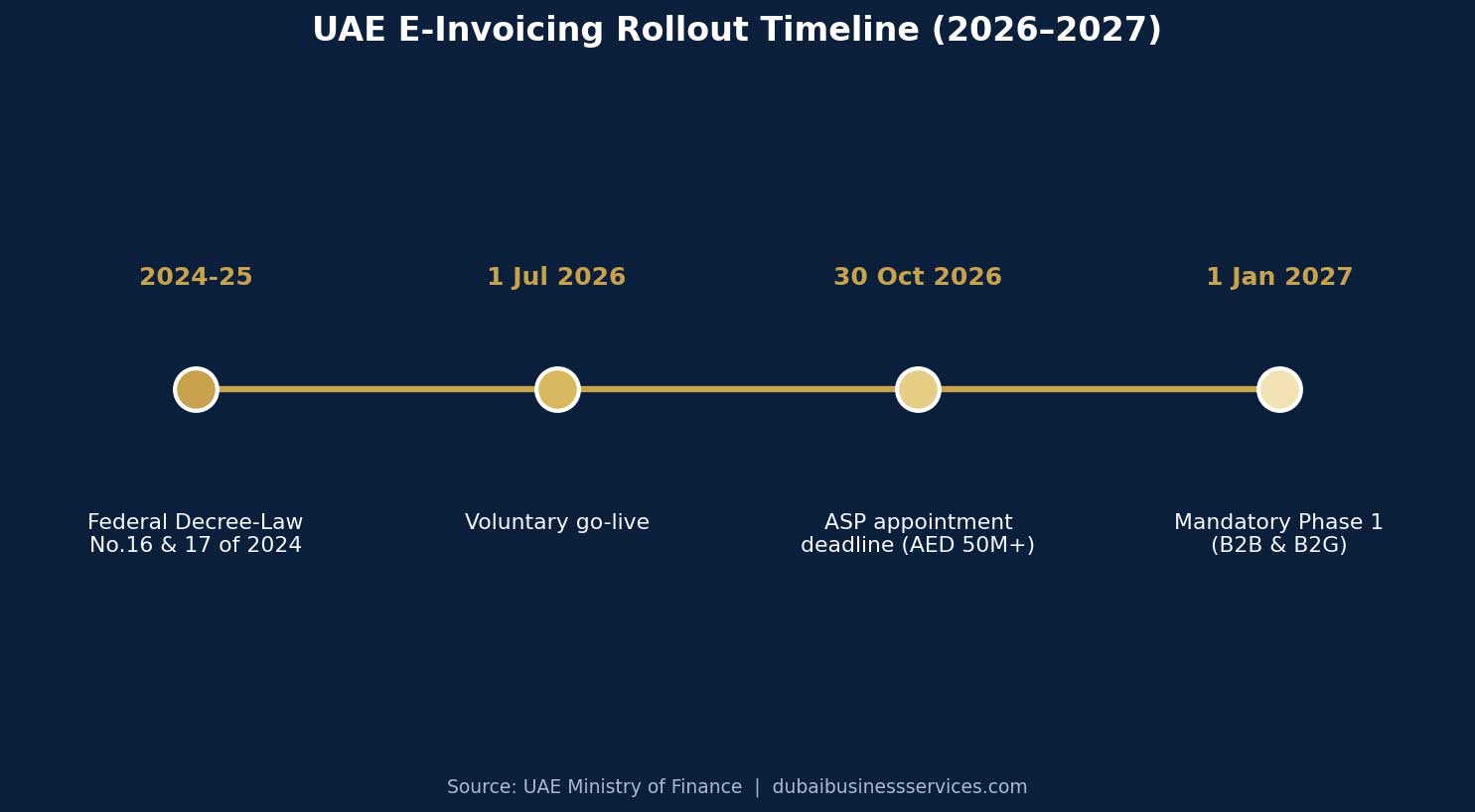

The Ministry of Finance updated the ASP appointment deadline for large businesses (AED 50M+ revenue) on 10 May 2026. The original deadline of 31 July 2026 has been extended to 30 October 2026. The mandatory go-live date of 1 January 2027 remains unchanged. This extension gives businesses a slightly longer window to select and onboard their ASP, but it does not change the need to start the process immediately. ERP adjustments, data mapping, and integration testing all take time that this extension does not replace.

The Rollout Timeline — Phase by Phase

The UAE e-Invoicing rollout follows a phased schedule set out in Ministerial Decision 244 of 2025. The pilot opens July 2026; mandatory compliance arrives in three waves through 2027.

The UAE has structured the e-Invoicing rollout into clear phases. Understanding exactly which phase applies to your business is the essential first step in building your implementation plan.

| Phase | Date | Who | ASP Appointment By | Go-Live |

|---|---|---|---|---|

| Pilot / Voluntary | 1 July 2026 | Any business meeting FTA technical requirements — participation is voluntary but must be agreed in writing | Before pilot participation | 1 July 2026 |

| Wave 1 — Large Business | 1 January 2027 | Businesses with annual revenue ≥ AED 50 million | 30 October 2026 | 1 January 2027 |

| Wave 2 — SMEs | 1 July 2027 | Businesses with annual revenue < AED 50 million (in scope) | 31 March 2027 | 1 July 2027 |

| Wave 3 — Government | 1 October 2027 | UAE government entities | 31 March 2027 | 1 October 2027 |

One important detail: businesses that participate voluntarily in the pilot phase from 1 July 2026 are not subject to penalties for non-compliance during that phase. The voluntary phase is explicitly a testing environment. However, once your mandatory go-live date arrives, penalties apply immediately and without a grace period.

What Makes a Valid UAE e-Invoice

The FTA's February 2026 technical guidance document specifies the complete set of mandatory data fields for UAE e-Invoices. The following categories of information must be present in every valid e-Invoice:

Mandatory Invoice-Level Fields

- Invoice number (unique identifier)

- Invoice issue date and time

- Invoice type code (tax invoice, commercial invoice, credit note, debit note)

- Currency code and exchange rate where applicable

- Supplier TIN (first 10 digits of corporate tax registration number)

- Supplier TRN (VAT registration number, where VAT-registered)

- Supplier legal name and address

- Buyer TIN and legal name

- Payment terms and due date

- Total amounts — taxable, tax amount, and gross total

Mandatory Line-Level Fields

- Line item identifier and description

- Unit of measure and quantity

- Unit price and line amount

- VAT category code (standard rate, zero rate, exempt)

- VAT rate percentage applicable to the line

- Line VAT amount

- Discount amount (if applicable)

- Invoice scenario classification (one of 16 defined scenarios)

The UAE system identifies 16 different invoicing scenarios, each with specific data requirements. Your business must correctly classify every transaction against the appropriate scenario. Misclassification can cause invoice rejection by the ASP before transmission even occurs. For businesses with complex transaction types — cross-border supplies, partial exemptions, reverse charge situations — this classification process requires careful review of the guidance and, in some cases, a VAT opinion.

One notable feature of the UAE system is that no QR code or barcode is required on UAE e-Invoices, unlike some other regional systems such as Saudi Arabia's ZATCA framework. The FTA's validation and tracking happens through the ASP network and the Tax Data Document rather than through a printed code.

Penalties for Non-Compliance

Businesses that participate voluntarily in the pilot phase are not subject to penalties during that phase. Once your Wave 1 or Wave 2 mandatory date arrives, however, penalties under Cabinet Decision No. 106 of 2025 apply immediately. There is no additional grace period after the mandatory go-live date.

| Violation | Penalty |

|---|---|

| Failure to implement the e-Invoicing system or appoint an Accredited Service Provider by the deadline | AED 5,000 per month |

| Each invoice or credit note not issued or transmitted on time through the system | AED 100 per document |

| Failure to notify the FTA of a system failure or outage within two business days | AED 1,000 per day |

| Failure to store electronic records in the UAE and make them accessible to the FTA | Administrative penalties under the Tax Procedures Law |

Records must be stored for five to seven years in an accessible electronic format within the UAE. This is not a trivial requirement for businesses that currently archive PDF invoices on local drives or external email. Your storage approach needs to be part of your e-Invoicing implementation plan, not an afterthought.

Your Practical Action Plan

ERP upgrades, ASP selection, data mapping, and staff training all take time. The businesses that start now will complete implementation without disruption. Those that wait may not.

The following steps apply to any UAE business in scope of the mandate. The sequence matters — some steps must precede others and the ASP selection and ERP work are often the longest lead-time items.

Step 1 — Confirm your scope and wave. Determine whether you fall in Wave 1 (AED 50M+ revenue, go-live 1 January 2027) or Wave 2 (<AED 50M, go-live 1 July 2027). Review Ministerial Decision 243 for any specific exclusion that might apply to your transaction types.

Step 2 — Assess your current invoicing process. Map every invoice type your business issues: standard VAT invoices, simplified invoices, credit notes, debit notes, self-billing arrangements. Identify which of the 16 UAE e-Invoicing scenarios each type falls under.

Step 3 — Conduct a technology gap assessment. Determine whether your current ERP or accounting software can generate PINT AE XML output. Major ERP providers (SAP, Oracle, Microsoft Dynamics) are building certified connectors, but your specific version and configuration may require upgrades or custom development.

Step 4 — Select and appoint your ASP. Review the FTA's list of accredited providers at tax.gov.ae. Evaluate compatibility, integration approach, support quality, and commercial terms. Wave 1 businesses must appoint their ASP by 30 October 2026.

Step 5 — Integrate and test. Work with your ASP to integrate your accounting system with the Peppol network, map your master data (TIN, supplier details, tax categories) to PINT AE fields, and conduct end-to-end testing before go-live.

Step 6 — Train your team. Finance staff, accounts receivable teams, and any staff involved in invoice processing need to understand the new workflow, what happens when an invoice is rejected, and how to respond to ASP error messages.

Step 7 — Consider the pilot. Joining the voluntary pilot from 1 July 2026 gives you a live testing environment with no penalty exposure. This is strongly recommended for Wave 1 businesses — completing a live pilot before your mandatory date reduces the risk of disruption significantly.

The businesses that will struggle are the ones treating e-Invoicing as an IT project to be addressed once the deadline is close. In practice, the combination of ERP upgrades, ASP onboarding, data cleansing, staff training, and testing takes three to six months for a business with a moderate transaction volume. Wave 1 businesses that have not begun their ERP assessment by July 2026 are at genuine risk of missing the January 2027 deadline.

1Stop Connect's accounting and compliance team can assist UAE businesses with scope assessment, process mapping, and coordination with ASPs and ERP consultants. If you are uncertain where to start or where your business stands, contact us directly — the initial assessment is complimentary.

"e-Invoicing is not a burden that arrived unexpectedly. It is the next step in a sequence of digital reforms that the UAE has been building deliberately since 2017. The businesses that treat it as a compliance project will comply. The businesses that treat it as an infrastructure upgrade — and use it to clean their data, streamline their processes, and reduce manual work — will come out of it in better shape than they went in."

— Dr. Dieter Hovorka, PhDFrequently Asked Questions

Is e-Invoicing mandatory in the UAE, and when? +

Yes. Under Ministerial Decisions No. 243 and 244 of 2025, e-Invoicing becomes mandatory in phases. Businesses with annual revenue of AED 50 million or more must go live by 1 January 2027 and appoint an Accredited Service Provider by 30 October 2026. Businesses below AED 50 million must go live by 1 July 2027. Government entities must comply by 1 October 2027. A voluntary pilot phase, open to any business meeting the FTA's technical requirements, launches on 1 July 2026.

Does e-Invoicing apply to my free zone company? +

Yes. The mandate applies to all persons conducting business in the UAE for B2B and B2G transactions, including companies in all UAE free zones — DIFC, DMCC, JAFZA, ADGM, and all others. The FTA has made clear that no exemptions will be granted based on free zone location or jurisdiction type. If you operate in a free zone and conduct B2B transactions, you are in scope unless a specific exclusion in Ministerial Decision 243 applies to your transaction type.

What happens to my current PDF invoices? +

PDF invoices, Word documents, scanned paper invoices, and email attachments will not be considered valid e-Invoices under the UAE mandate from your applicable go-live date. All B2B and B2G invoices must be structured XML files in the PINT AE format, transmitted through an Accredited Service Provider. Continuing to issue PDFs after your mandatory date will trigger penalties of AED 100 per invoice not transmitted correctly through the system.

Do I need e-Invoicing if I am not VAT-registered? +

Potentially yes. The scope of the mandate under Ministerial Decision 243 is wider than VAT — it applies to "all persons conducting business in the UAE" for their B2B and B2G transactions, whether or not they are VAT-registered. There are specific exclusions, but being below the VAT threshold is not in itself an exclusion from e-Invoicing. You should review your situation against the specific exclusions listed in Ministerial Decision 243 and, where in doubt, take professional advice.

What does an Accredited Service Provider actually do? +

Your ASP is the intermediary between your accounting system and the rest of the Peppol network. It receives your invoice data in XML format, validates it against PINT AE specifications and FTA mandatory field requirements, transmits it to your buyer's ASP through the Peppol network, and reports a Tax Data Document to the FTA (Corner 5) in near real time. It also returns a Message Level Status confirming whether the transmission was successful or identifying errors. Without an ASP, your invoices cannot be validly issued or received under the UAE e-Invoicing system.

What are the penalties for not implementing e-Invoicing on time? +

Under Cabinet Decision No. 106 of 2025: AED 5,000 per month for failure to implement the system or appoint an ASP by the deadline; AED 100 per invoice or credit note not issued or transmitted correctly; AED 1,000 per day for failure to notify the FTA of system failures within two business days. Records not stored in the UAE in accessible electronic format for five to seven years may attract additional penalties under the Tax Procedures Law. Penalties apply from your mandatory go-live date — there is no additional grace period.