Why "Build Your Castle"?

A castle isn't just a building. It's a fortress. Walls designed to withstand siege. Moats to keep attackers at distance. Multiple layers of defense. Strategic positioning on high ground.

Your wealth deserves the same architectural thinking.

A St. Kitts & Nevis trust, specifically a Nevis trust under the Nevis International Exempt Trust Ordinance (NIETO), is that castle. It's not the only offshore trust jurisdiction. But it's the fortress. The structure specifically engineered to resist creditor attacks, legal challenges, and forced heirship claims with a level of protection unmatched globally.

This isn't theory. This is legislated asset protection that has been tested in courts, refined over decades, and stands as one of the strongest legal structures available to protect generational wealth.

"The best time to build your fortress is before the storm. Asset protection works when it's in place before the claim arises."

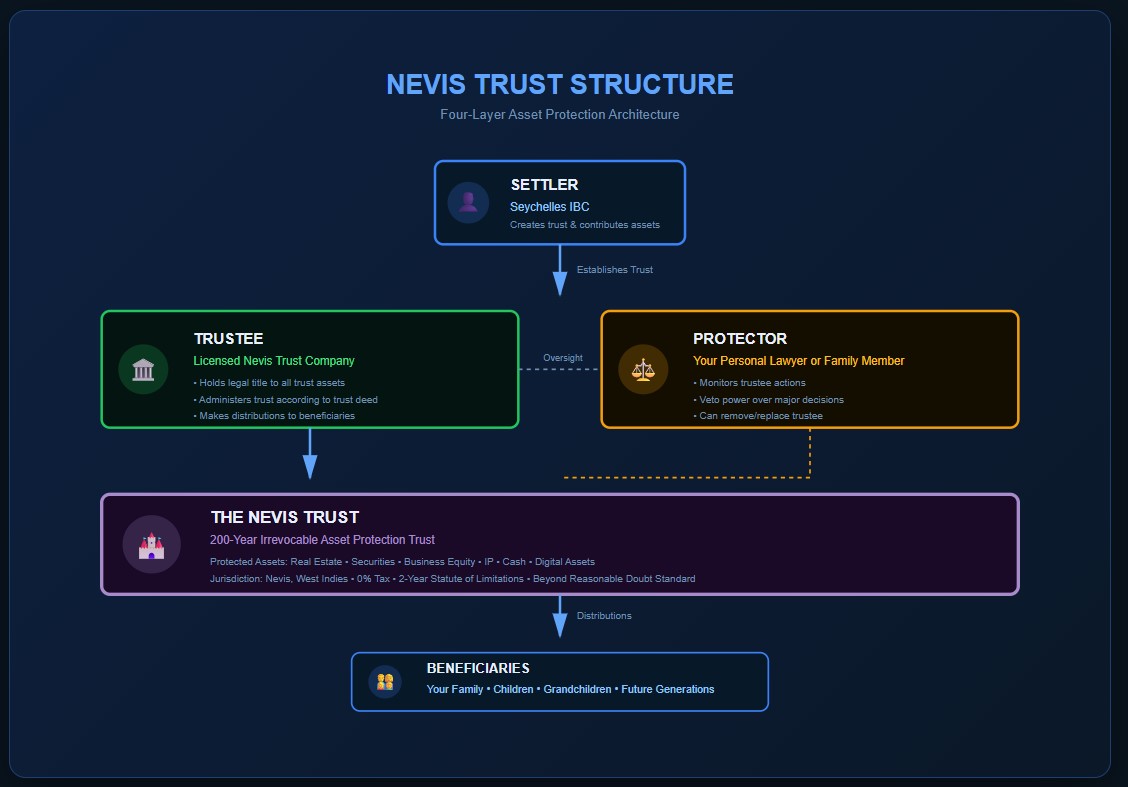

— Offshore trust practitioners' axiomThe Four Key Players: Understanding Trust Roles

Before we discuss why Nevis is superior, you need to understand how trusts actually work. A trust isn't a company. It's not an account. It's a legal relationship between four parties, each with distinct roles and responsibilities.

The Settler (Grantor / Trustor)

This is you. The person creating the trust and contributing assets to it.

What the settler does: Establishes the trust by signing a trust deed. Transfers assets into the trust (real estate, securities, cash, IP, etc.). Defines who the beneficiaries are. Outlines the purpose and terms of the trust.

What the settler cannot do (in an irrevocable trust): Once assets are transferred, the settler loses direct control. You cannot unilaterally withdraw assets. You cannot change beneficiaries without trustee/protector consent. This loss of control is what creates the protection, if you don't control it, creditors can't reach it.

Tax residency matters: The settler's tax residency determines reporting obligations. A US settler faces different rules than a Seychelles IBC acting as settler.

Many sophisticated structures use an offshore company (Seychelles IBC, BVI company, or similar) as the settler rather than an individual. This adds a corporate layer, separates the individual from direct trust creation, and can provide additional tax and privacy benefits depending on jurisdiction.

The Trustee

This is the entity that holds legal title to the trust assets and administers the trust according to its terms.

Legal requirement in Nevis: The trustee must be a licensed Nevis trust company. You cannot act as your own trustee. This is a regulatory requirement and a protective feature, having a professional, licensed, locally regulated trustee strengthens the legal validity of the trust structure.

What the trustee does: Holds legal title to all trust assets. Makes distributions to beneficiaries according to the trust deed. Invests and manages trust assets prudently. Maintains trust records and accounts. Ensures compliance with Nevis trust law. Files annual trust returns with the Nevis authorities (confidential, not public).

Fiduciary duty: The trustee owes a fiduciary duty to the beneficiaries. This means acting in their best interest, managing assets prudently, avoiding conflicts of interest, and following the terms of the trust deed. This duty is legally enforceable.

Having a professional Nevis-licensed trustee is not bureaucratic overhead. It is a critical layer of defense. Courts recognize licensed trustees as legitimate. Creditors cannot claim the trust is a sham if a regulated third-party is administering it according to law.

The Protector

This is the optional (but highly recommended) supervisory role. Think of the protector as the guardian overseeing the trustee.

Who can be a protector: Your personal lawyer. A trusted family member. A law firm. An accountant. The protector can be anyone you trust, there is no licensing requirement for protectors in Nevis.

What the protector does: Monitors the trustee's actions. Approves or vetoes certain trustee decisions (investment changes, distributions, amendments). Can remove and replace the trustee if necessary. Ensures the trust is being administered according to your intent.

Why you want a protector: Without a protector, the trustee has full discretion within the trust terms. With a protector, you retain indirect influence. The protector acts as your eyes and voice without giving you direct control (which would undermine asset protection). This is the balance: you don't control the assets, but you have oversight through a trusted person.

The Beneficiaries

These are the people (or entities) who receive the benefit of the trust assets.

Types of beneficiaries: Named beneficiaries: explicitly listed in the trust deed (your children, spouse, etc.). Class of beneficiaries: defined by category ("my descendants," "my family members"). Discretionary beneficiaries: the trustee has discretion over who receives distributions and when.

Rights of beneficiaries: Entitled to distributions according to the trust terms. Can request information about the trust (though this varies based on trust structure). Can take legal action if the trustee breaches fiduciary duty.

Flexibility: You can be a beneficiary of your own trust. But this creates tax and creditor implications depending on your residency. Many structures exclude the settler as a beneficiary to maximize protection.

Why Nevis is Stronger Than Everywhere Else

Asset protection trusts exist in many jurisdictions. Cook Islands, Belize, Cayman Islands, BVI, Seychelles, even US states like Delaware and South Dakota. Switzerland and Luxembourg offer trusts. So why Nevis?

Because Nevis trust law was purpose-built for asset protection and has been refined over 30 years specifically to resist creditor attacks. Let's compare.

Nevis vs Cook Islands

Cook Islands trusts are often cited as the gold standard for asset protection. They're good. But Nevis is better on several key metrics.

| Factor | Nevis | Cook Islands |

|---|---|---|

| Statute of Limitations | 2 years from asset transfer | 4 years (1 year if creditor knew of transfer) |

| Burden of Proof | Beyond reasonable doubt (criminal standard) | Beyond reasonable doubt |

| Recognition of Foreign Judgments | Not recognized without retrial in Nevis | Not recognized without retrial |

| Legal Costs for Creditor | Must hire Nevis lawyer, post bond, prove fraud in Nevis court | Must hire Cook Islands lawyer, post bond |

| Trust Duration | Up to 200 years | Typically 125 years |

Verdict: Nevis wins on statute of limitations (2 years vs 4 years) and trust duration (200 years vs 125 years). Both have equivalent criminal burden of proof and rejection of foreign judgments. Nevis is faster to become unassailable.

Nevis vs Switzerland

Switzerland has a reputation for privacy and wealth management. Swiss trusts exist but are fundamentally different from Nevis trusts.

Nevis Advantages

- No forced heirship. Nevis does not recognize forced heirship rules. You can disinherit anyone. Swiss law imposes forced heirship—portions of your estate must go to certain heirs regardless of your wishes.

- Tax-free. No tax on trust income or assets in Nevis. Switzerland taxes trust income depending on structure and beneficiary residence.

- Asset protection focus. Nevis trust law explicitly designed to defeat creditors. Swiss trusts follow traditional common law without specific anti-creditor provisions.

- No CRS automatic exchange (for trusts). Nevis trusts are not financial accounts and fall outside CRS automatic exchange in most structures. Swiss banks report under CRS.

Switzerland Advantages

- Banking access. Swiss banks are easier to access for trust structures than Nevis. Nevis trusts typically bank in third jurisdictions (Cayman, Singapore, etc.).

- Brand recognition. "Swiss trust" carries historical prestige in wealth management circles.

- Stability. Switzerland is politically stable, economically strong, and institutionally mature for centuries.

Verdict: For asset protection, Nevis is categorically stronger. Switzerland is better for wealth management and banking relationships, but not for creditor defense.

Nevis vs Luxembourg

Luxembourg trusts are relatively recent (introduced 2003) and designed primarily for estate planning in the EU context.

Why Luxembourg loses: EU member state, subject to EU regulations, CRS reporting, potential EU-wide judgments. Forced heirship applies under Luxembourg law. No specific asset protection statutes like Nevis. Trust income may be taxable depending on structure.

Why Luxembourg exists: For EU-resident individuals who want a trust structure without leaving the EU regulatory environment. For estate planning, not asset protection.

Verdict: Not comparable. Luxembourg trusts serve a different purpose. For hardcore asset protection, Nevis wins decisively.

Nevis vs BVI

BVI offers trusts under the BVI Trustee Act and VISTA (Virgin Islands Special Trusts Act) for holding shares.

BVI trust advantages: Well established offshore jurisdiction. Strong privacy laws. VISTA trusts useful for private equity and venture capital structures. No tax on trust income or gains.

Why Nevis is stronger: BVI does not have a specific fraudulent transfer statute for trusts with the same protective features as Nevis NIETO. BVI courts can apply common law fraudulent transfer principles which are less protective. Nevis statute explicitly designed to defeat creditors, BVI trusts rely on general offshore trust principles. Nevis: 2-year statute of limitations. BVI: no statutory limitation, creditors can challenge under common law indefinitely (though practically difficult).

Verdict: Nevis legislation is more explicitly protective. BVI is excellent for corporate structures (companies, funds) but Nevis is purpose-built for trusts.

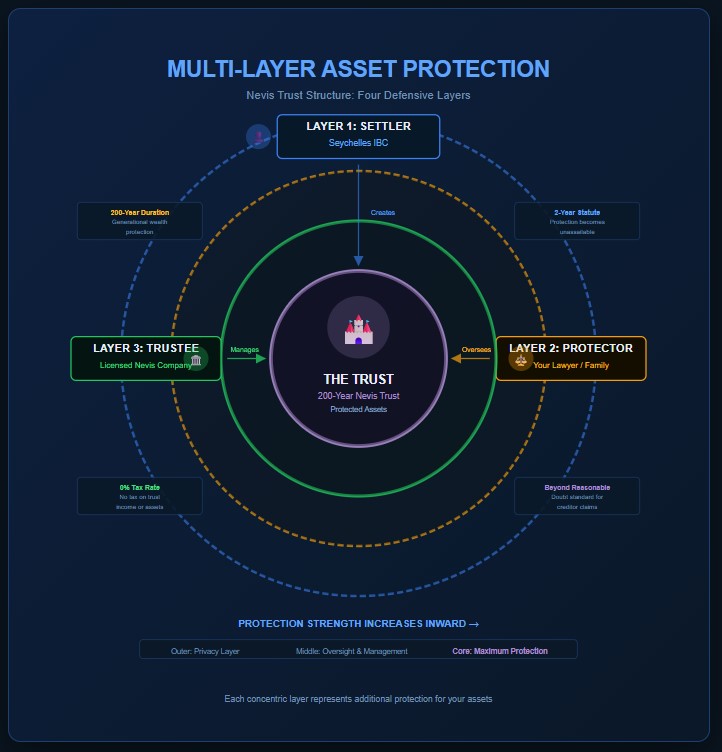

Nevis trust law was written specifically to protect assets from creditors. The 2 year statute of limitations, the beyond reasonable doubt burden of proof, the non-recognition of foreign judgments, these aren't accidents. They are legislative choices designed to make Nevis the fortress jurisdiction. Cook Islands did this too. But Nevis went further with a shorter statute and 200 year duration.

What Assets Can You Protect in a Nevis Trust?

Almost anything that can be legally owned can be placed in a Nevis trust. The trustee holds legal title. You (or your beneficiaries) retain the economic benefit.

Real Estate

Residential property. Commercial property. Land. Agricultural holdings. Rental properties.

How it works: The trustee holds title to the property. The trust deed specifies how rental income is distributed, when property can be sold, and who benefits. If properly structured before a claim arises, creditors cannot force sale of the property to satisfy a judgment against you personally.

Tax considerations: Rental income may be taxable in the jurisdiction where the property is located. The trust structure doesn't eliminate property taxes or income taxes on rental income—but it does protect the asset from seizure.

Securities and Investments

Publicly traded stocks. Bonds. Mutual funds. ETFs. Brokerage accounts.

How it works: Securities are transferred to a brokerage account in the name of the trust. The trustee manages or directs management. Dividends and capital gains accrue to the trust and can be distributed to beneficiaries or reinvested.

Flexibility: You can grant the protector power to direct investment decisions while the trustee maintains legal ownership. This allows you indirect control over investment strategy without compromising asset protection.

Private Business Equity

Shares in private companies. LLC membership interests. Partnership interests.

How it works: Transfer equity to the trust. The trustee becomes the shareholder/member. You can structure operating agreements or shareholder agreements to give you management control while the trust owns the equity. This separates operational control from ownership, you run the business, the trust owns it.

Strategy: Particularly powerful for family businesses. The business continues operating under your direction, but creditors cannot seize equity held by the trust.

Intellectual Property

Patents. Trademarks. Copyrights. Trade secrets (if documentable).

How it works: The trust becomes the registered owner of the IP. The trust licenses the IP back to you or your operating companies. Royalty income flows to the trust. This protects valuable IP from creditor claims while allowing you to continue using and commercializing it.

Cash and Precious Metals

Bank deposits. Gold, silver, platinum holdings. Cryptocurrency (if properly custodied).

How it works: The trustee opens bank accounts in the trust name. Physical metals held by custodian in trust name. Cash transferred into trust accounts.

Liquidity benefit: Unlike real estate or business equity, cash and metals in trust can be quickly distributed to beneficiaries or used for investments without complex legal transfers.

Digital Assets

Cryptocurrency wallets. NFTs. Digital businesses. Online accounts with transferable value.

How it works: Transfer custody of private keys to trustee or multi-signature wallet requiring trustee approval. Digital asset exchanges can open accounts in trust name (not all exchanges allow this, check requirements).

Emerging area: Trust law is catching up to digital assets. Nevis trust law does not explicitly exclude digital assets, so they can be held, but practical custody and management remain complex.

Assets already subject to a legal claim. If a lawsuit is filed or a judgment exists, transferring assets to a trust afterward is a fraudulent transfer and courts will reverse it. Asset protection must be proactive, not reactive.

Assets you need direct daily control over. If you transfer your operating company to a trust but continue acting as if it's yours (signing contracts in your own name, commingling funds), courts may pierce the trust as a sham. The structure must be real.

Illegal assets. Obviously, you cannot protect proceeds of illegal activity or assets obtained through fraud.

Building Your Structure: The Recommended Setup

Here's the structure we recommend for sophisticated asset protection, combining maximum privacy, legal defensibility, and flexibility.

Layer 1: The Settler (Seychelles IBC)

Instead of you personally acting as settler, establish a Seychelles International Business Company (IBC) to be the settler.

Why Seychelles? Zero tax on offshore income. Strong privacy laws (beneficial ownership not public). No public registry of shareholders or directors. Fast and inexpensive to establish. Stable legal system based on English common law.

How it works: You own the Seychelles IBC (via nominee shareholders if desired for added privacy). The Seychelles IBC creates the Nevis trust and contributes assets to it. This adds a corporate layer between you and the trust, enhancing both privacy and legal insulation.

Layer 2: The Trustee (Licensed Nevis Trust Company)

The trustee must be a Nevis-licensed trust company. These are regulated by the Nevis Financial Services Regulatory Commission.

Selecting a trustee: Look for experience (how long operating), regulatory compliance (licensed and in good standing), fee structure (annual admin fees vary), and reputation (check references, track record).

What the trustee does: Holds legal title to all trust assets. Opens and manages bank accounts in the trust name. Makes distributions to beneficiaries. Files annual Nevis trust returns (confidential). Maintains trust records and accounts.

Layer 3: The Protector (Your Personal Lawyer or Family Member)

Appoint a protector to oversee the trustee and retain indirect influence over the trust.

Best choice: Your personal lawyer. Lawyer-client privilege may apply to communications. Professional oversight and fiduciary competence. Independent from the trustee (avoids conflicts of interest).

Alternative: Trusted family member. Adult child, sibling, spouse, or close advisor. Must be someone you trust completely and who understands their fiduciary responsibilities.

Powers to grant the protector: Veto power over trustee investment decisions. Approval required for distributions above a certain threshold. Authority to remove and replace the trustee. Consent required for amendments to the trust deed.

What the protector cannot do: Directly access or withdraw trust assets (that would undermine protection). Act in their own interest rather than beneficiaries' interests (fiduciary duty). Make decisions that contradict the trust deed.

Layer 4: The Trust Itself (200-Year Irrevocable Nevis Trust)

Why 200 years? Generational wealth protection. The trust can span multiple generations, your children, grandchildren, great-grandchildren. Long-term asset accumulation without forced liquidation. Avoids probate in perpetuity, assets never pass through your estate or beneficiaries' estates.

Irrevocable vs Revocable: Revocable trusts offer no asset protection, if you can revoke it, creditors can force you to revoke it. Irrevocable trusts provide protection because you genuinely give up control. This is the trade off: protection requires relinquishing direct control.

Discretionary distributions: The trust deed should grant the trustee discretion over distributions. This prevents creditors from claiming a beneficiary has a fixed, enforceable right to distributions (which creditors could seize). Discretion equals protection.

You establish a Seychelles IBC (you own it via nominee shareholders for privacy). The Seychelles IBC creates a Nevis trust and contributes $5M in securities and real estate. The Nevis trust is administered by a licensed Nevis trustee. Your personal lawyer is the protector with veto power over major decisions. Beneficiaries are your spouse and children. After 2 years (statute of limitations expires), the structure is essentially unassailable by future creditors.

Why 1Stop Connect is the First Address for Nevis Trusts

Establishing a trust isn't like opening a bank account. It requires legal expertise, understanding of international tax law, coordination across jurisdictions, and relationships with licensed trustees.

We've been doing this since 1998. Over 25 years establishing offshore structures including Nevis trusts, Seychelles IBCs, Cook Islands trusts, and multi-jurisdictional asset protection strategies.

We know the trustees. We work with licensed Nevis trust companies we've vetted over decades. We know their fee structures, their responsiveness, their compliance standards. We introduce you to the right trustee for your situation.

We structure the layers correctly. Settler selection (individual vs IBC), protector appointment (lawyer vs family member), beneficiary designation (fixed vs discretionary), asset transfer strategy (timing, valuation, documentation), every detail matters. We get it right.

We integrate with your existing planning. Tax advisors, estate planners, wealth managers, a Nevis trust doesn't exist in isolation. We coordinate with your existing advisors to ensure the trust complements your overall financial and estate plan.

We maintain the structure. Annual trustee fees, Nevis compliance filings, protector oversight, beneficiary distributions, trusts require ongoing administration. We provide continuity and support for the life of the trust.

We are based in Nevis. Registered and licensed in the jurisdiction. Direct relationships with Nevis trust companies, Nevis legal counsel, and Nevis regulatory authorities. When you work with us, you're working with people who live and operate in the ecosystem. Not someone marketing Nevis trusts from Europe or North America. We're here.

Final Thoughts: Asset Protection is Not Evasion

Building a Nevis trust is legal. Protecting assets from future creditor claims is legal. Structuring wealth to survive across generations is legal.

What's not legal: transferring assets to a trust after a lawsuit is filed (fraudulent transfer). Hiding assets to evade legitimate judgments (fraud). Using a trust to evade taxes (tax evasion).

Asset protection works when it's done in advance, structured correctly, administered professionally, and maintained with integrity. It is a defensive strategy, not an offensive weapon. The goal is to make litigation against you economically irrational for creditors because the cost and difficulty of piercing the structure exceeds any potential recovery.

A well structured Nevis trust achieves this. It creates a legal fortress that is expensive to attack, difficult to breach, and ultimately not worth the effort for most creditors. That's not evasion. That's smart wealth planning.

Build your castle. Protect what you've built. Make it generational.

This article provides general information about Nevis trusts and asset protection structures. It is not legal or tax advice. Trust law, asset protection law, and tax law vary significantly by jurisdiction and individual circumstances.

You must engage qualified legal and tax advisors in both your home jurisdiction and in Nevis before establishing any trust or offshore structure. The information provided here is current as of January 2026 but laws change. Professional advice tailored to your specific situation is essential.

If you would like to discuss your specific situation and explore whether a Nevis trust makes sense for your asset protection and estate planning goals, contact 1Stop Connect. We are here to help you build the right structure.